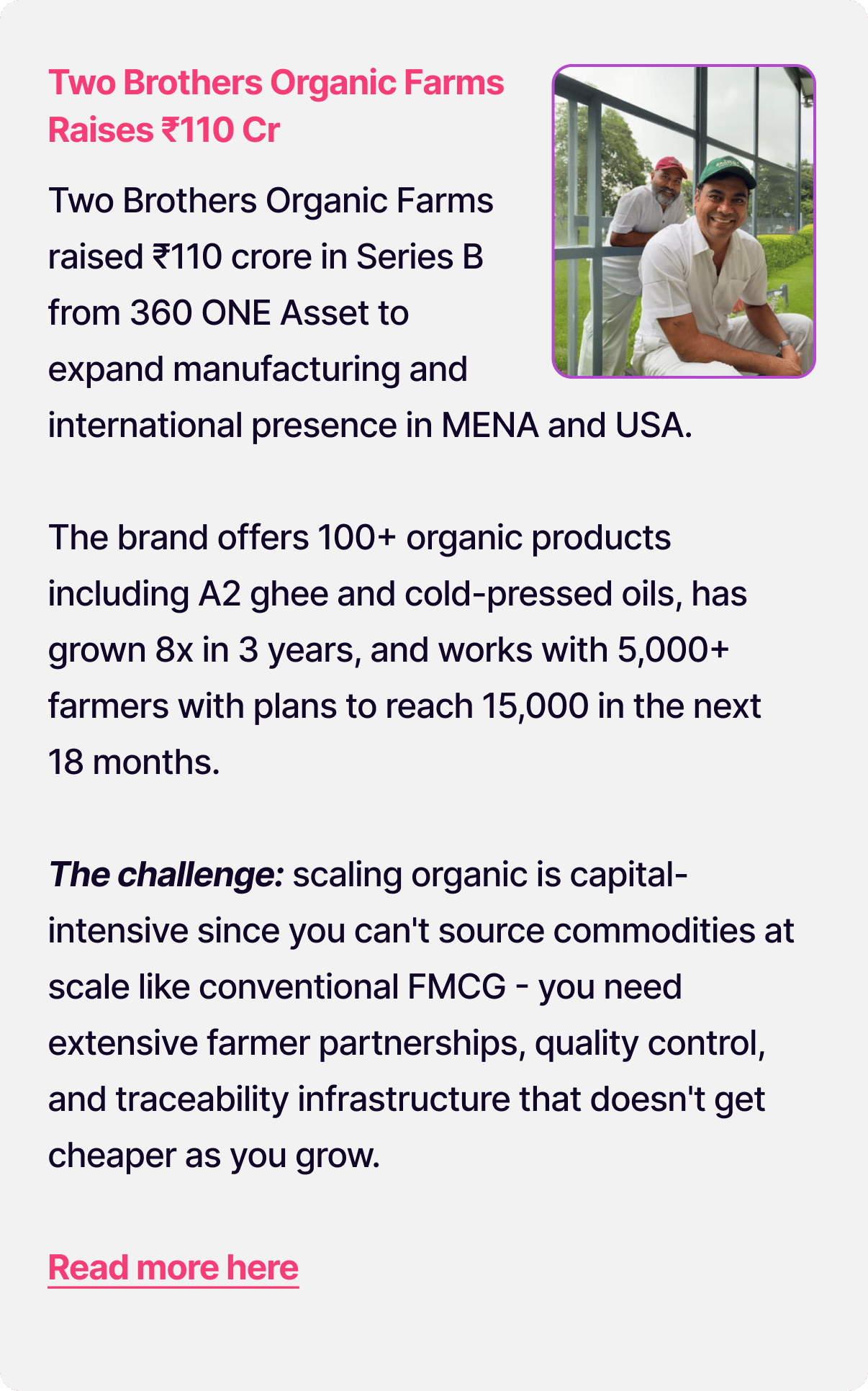

- Merito

- Posts

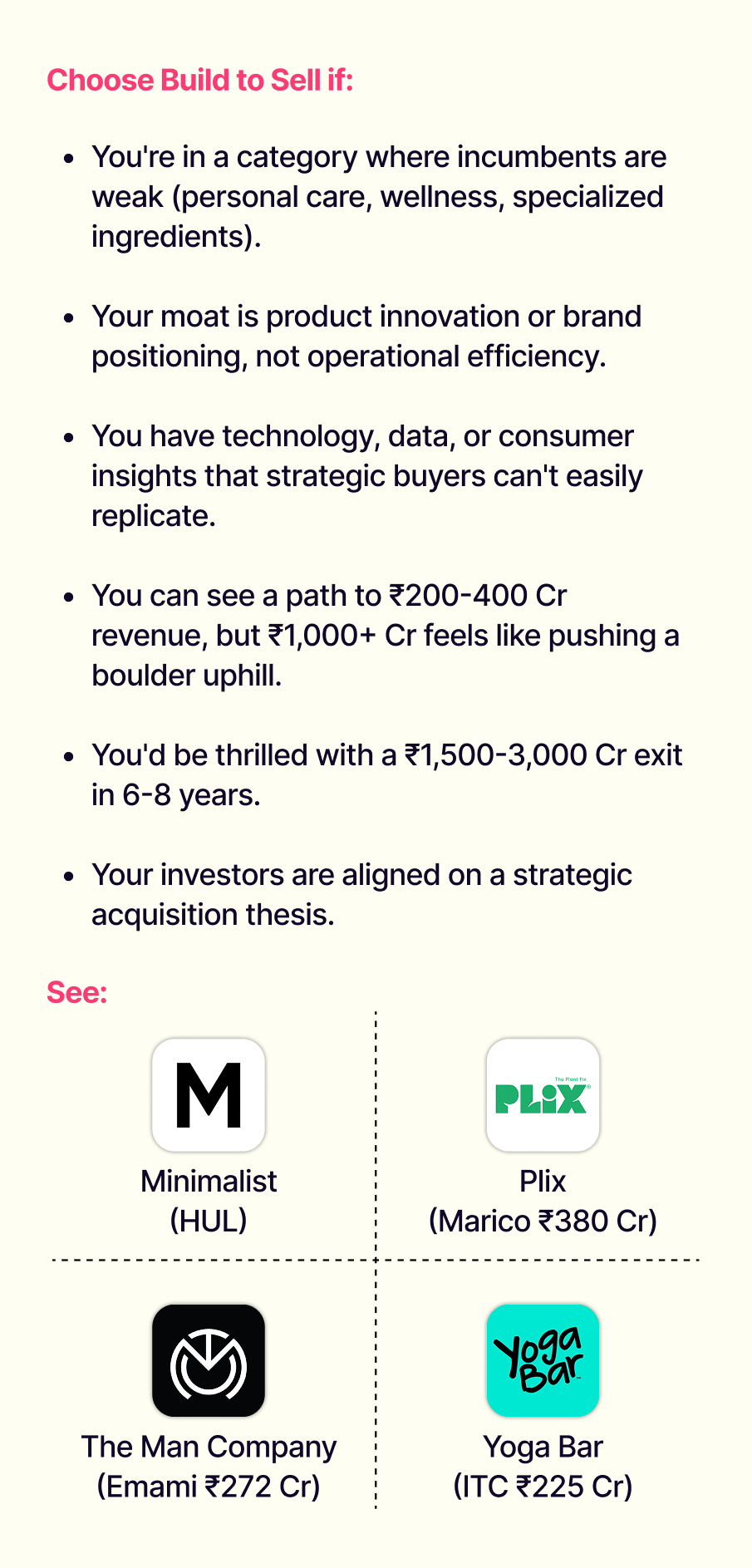

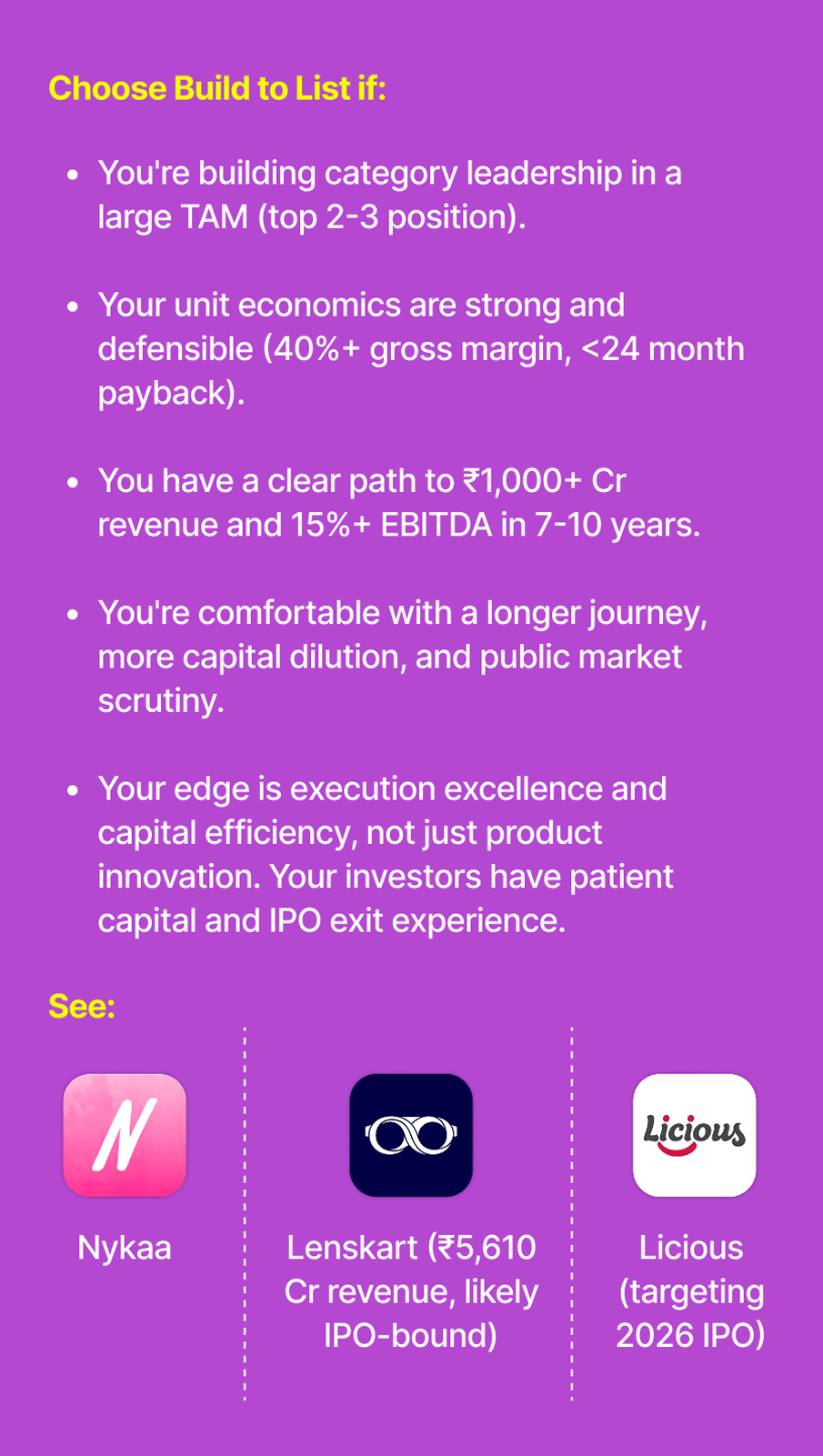

- Building to Sell or List?

Building to Sell or List?

The Decision You Must Make at ₹50 Crore, Not ₹500 Crore

D2C x Sell or Build

Hey readers,

Welcome to the Eleventh edition of D2C Cents!

TLDR - We are your scroll-friendly, no-fluff download of what's shaping India's D2C brands.

This edition? We talk about:

Strategies D2C founders must adopt for a best-case scenario in an acquisition v/s listing

The sharpest D2C news that matters

So, like, in Jan 2025, HUL bought this tiny company called Minimalist for ₹2,955 crore. The company barely made money, only ₹10 crore profit on ₹347 crore sales. But HUL still paid a super big price, about 8.5 times their sales!

Then, in Aug 2025, BlueStone, a way bigger company, did its IPO. They had ₹1,770 crore sales, 275 stores, all over India. But the market said “nah” and gave them a price lower than the IPO. It listed at ₹510 against the ₹517 IPO price, a -1.4% listing loss. Even though they were 5 times bigger than Minimalist!

Same country. Same year. Totally different outcomes.

Moral? Tiny, not-so-profitable companies can get crazy expensive in buys, but bigger, growing ones can still struggle in the stock market.

It's a signal, and most D2C founders are reading it wrong.

So… only 14% of D2C brands in India actually make money. Out of 170+ brands in FY23, just 24 made profits. Yet, most founders are trying to build their biz to go public like, IPO style which needs big money, huge scale, and super predictable stuff.

You know what’s harsh? Less than 15% of D2C brands even make ₹250 crore before getting bought. And still, most founders are spending tons of cash trying to hit ₹1,000 crore so they can go IPO.

Math says: you’ll probably get bought. Your plan says: IPO. That clash? Yeah… it wrecks value at the worst time.

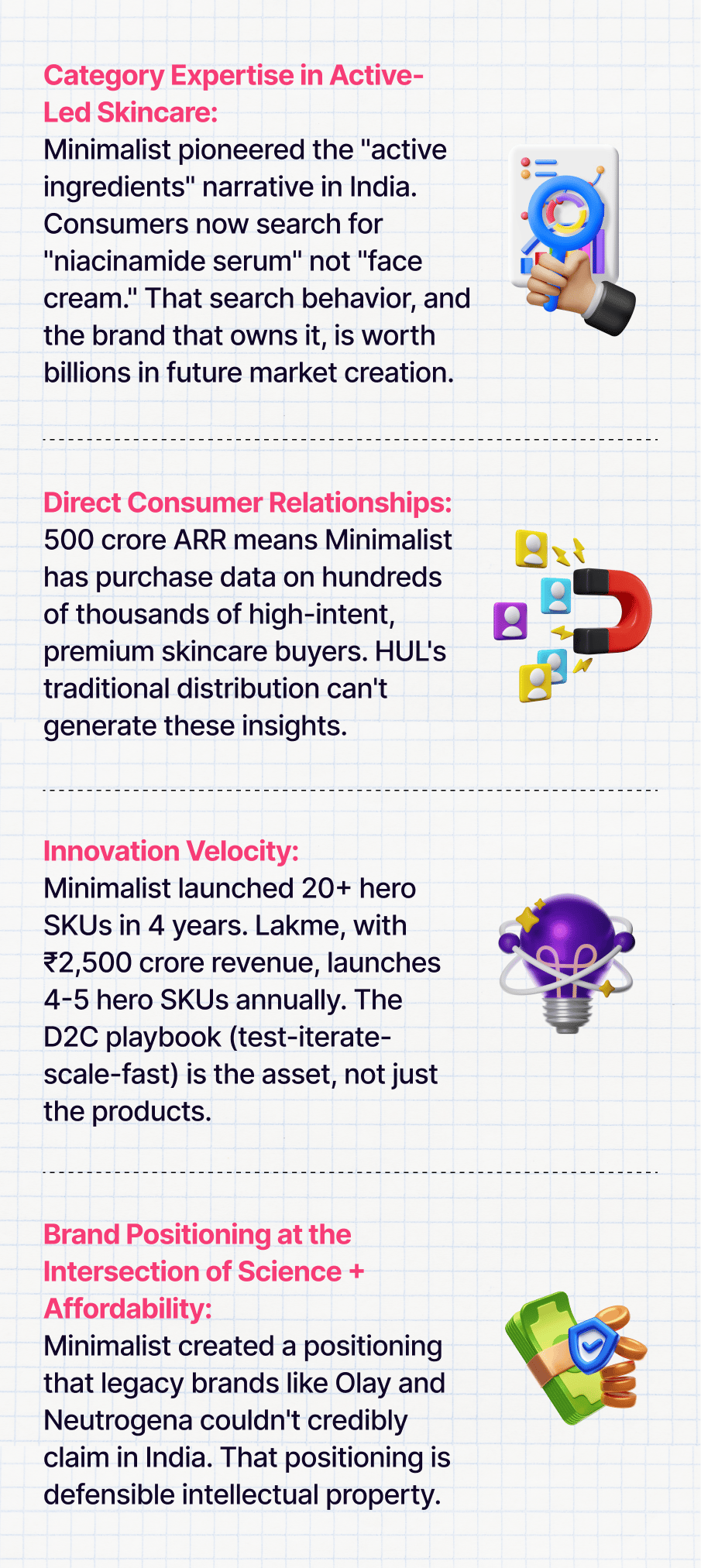

Let's understand why HUL paid 8.5x revenue for a brand that’s not yet profitable.

Strategic buyers don't buy revenue. They buy capability.

Here’s what HUL got with Minimalist:

HUL didn't pay for Minimalist's P&L. They paid for capabilities that would take them 5-7 years and ₹500+ crore to build internally.

What Public Markets Punish

BlueStone is an incredible business. They did ₹1,770 crore sales, have 275 stores, growing super fast, 64% more than last year, and 44% of customers keep coming back. They’re the 2nd biggest jewellery brand that’s both online and offline.

And the market gave it a muted reception.

Why?

Public markets don't reward "growth potential." They reward predictable cash generation. They care about cash coming in now. BlueStone lost ₹221 crore in FY25 (up from ₹142 crore). Even though they sold more, they lost MORE money.

For public market investors, that's not a growth story, it's a capital consumption story. Investors are like: “When will you make real cash? What's the path to 15%+ EBITDA margins?"

Once you’re selling ₹1,000+ crore, you’ve made a ton of choices that stick. You can’t suddenly switch from “Build to Sell” to “Build to List” halfway. Your company’s personality is already set.

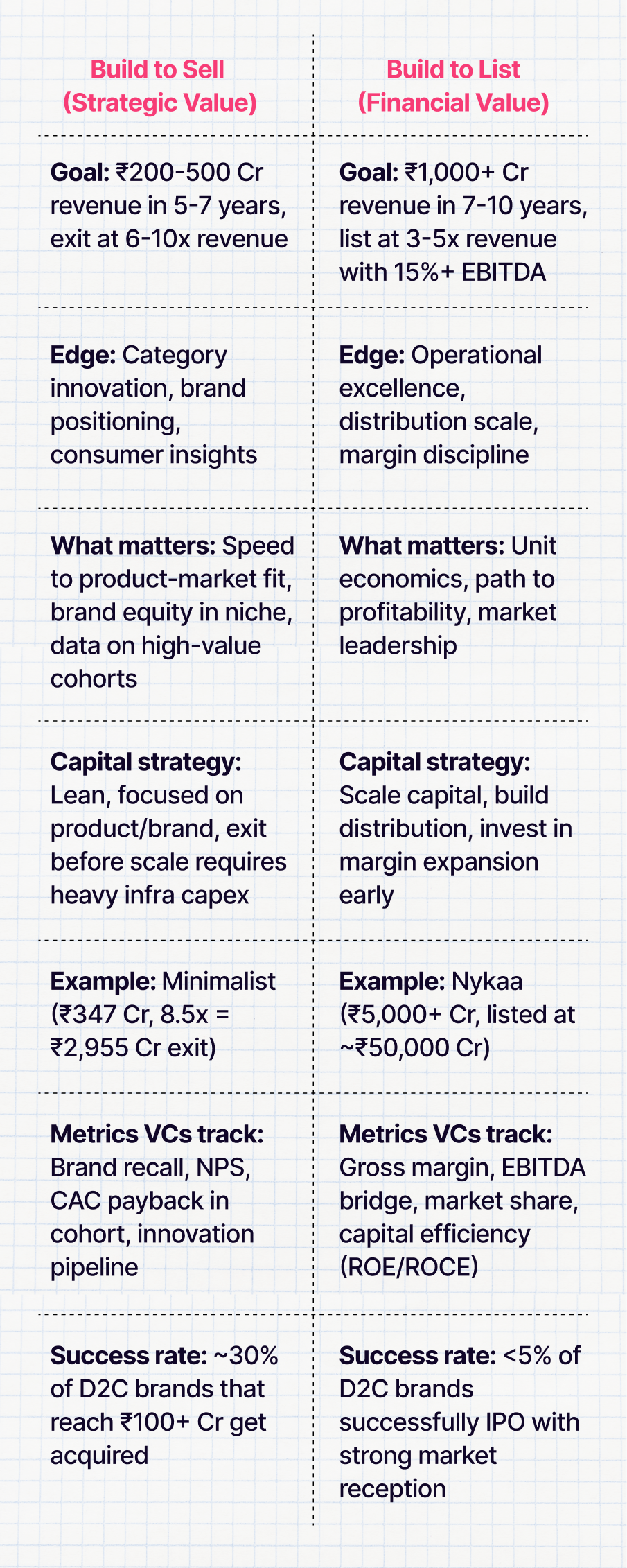

The Two Divergent Business Models

Most founders are building a hybrid, optimizing for neither. And that's the real capital destroyer.

Why ₹50 crore? Because that's when three things happen:

1. Capital Structure Crystallizes

If your lead investors are signaling "build to $1B+ valuation for IPO," you're already on the IPO path.

If your investors are saying "prove the model, we'll back you to ₹250 crore and find a strategic exit," you're on the acquisition path.

Your investors' return expectations dictate your business model.

If they want 10x on ₹50 crore (so a ₹500 crore exit), that screams strategic acquisition. If they want ₹2,000 crore exit… IPO math it is. Your company isn’t free to choose, it’s kinda tied to their expectations.

2. Talent and Org Structure Diverge

Build to Sell hires: product ninjas, brand storytellers, growth hackers, data scientists who understand consumer behaviour.

Build to List hires: finance heavyweights, supply chain experts, regional sales heads, CFOs who can drive margin expansion.

3. Innovation vs. Efficiency

By ₹50 crore, the game changes:

You gotta pick: keep inventing the next cool product (Build-to-Sell), OR make your processes super efficient to grow big margins (Build-to-List).

At ₹200 crore, that choice is almost impossible to undo.

So basically, the decision you make at ₹50 crore sets the future path for your company at ₹300 crore. Your exit options, your growth style, your whole company DNA… locked in.

The Framework: Which Path Should You Choose?

The Real Question

It's not "Will we IPO or get acquired?"

It's "Are we building the right business for our most likely outcome?"

That decision, made consciously at ₹50 crore, is worth 10x more than any growth hack at ₹500 crore.

Because by ₹500 crore, you're not choosing a path anymore. The path has chosen you.

What do you think? Are you building the right business model for your likely exit?

See you next edition - same time, deeper insights.

Until then, keep building strategically.

Abhishek